How to Buy Life Insurance in Pakistan: Step-by-Step Guide

Life insurance isn’t just for the wealthy or elderly; it’s a smart safety net for every Pakistani family. Whether you're a young professional in Lahore, a small business owner in Karachi, or a homemaker in Peshawar, securing your loved ones’ future starts with one decision: getting insured.

Whether you're buying your first policy or reviewing an existing one, this guide is your complete, step-by-step companion to making confident, informed choices because protecting your family shouldn’t be complicated.

Simple, Step-by-Step Process

Step 1: Understand What Kind of Life Insurance You Need

Not all policies are equal. In Pakistan, you mainly have two types:

Term Life Insurance:

●Pure protection: Pays a lump sum only if you pass away during the policy term (e.g., 10–30 years).

●Best for: Budget-conscious families, young earners, debt holders (e.g., home/car loans).

●Example: Pay Rs. 1,500/month for Rs. 5 million coverage until age 60.

Whole Life / Endowment Plans:

A mix of insurance and savings/investment. Pays out on death or at policy maturity.

●Best for: Long-term goals (such as a child’s education or retirement), those seeking forced savings.

●Note: Returns are modest (~5–7% p.a.), don’t treat it as a high-return investment.

Islamic Alternative? Choose Takaful:

SECP-licensed Takaful operators offer Shariah-compliant coverage based on cooperation, not interest or gambling: same protection, Halal structure.

Step 2: Calculate How Much Coverage You Need

A common mistake? Underinsuring. Use this simple “DIME” formula (Debt + Income + Mortgage + Education):

|

Component

|

Example

|

|

Debt (loans, credit cards)

|

Rs. 2 million

|

|

Income replacement (5–10 years)

|

Rs. 80,000/month × 120 months = Rs. 9.6 million

|

|

Mortgage/home loan

|

Rs. 6 million

|

|

Education (2 kids × Rs. 2M)

|

Rs. 4 million

|

|

Total Needed

|

~Rs. 21.6 million

|

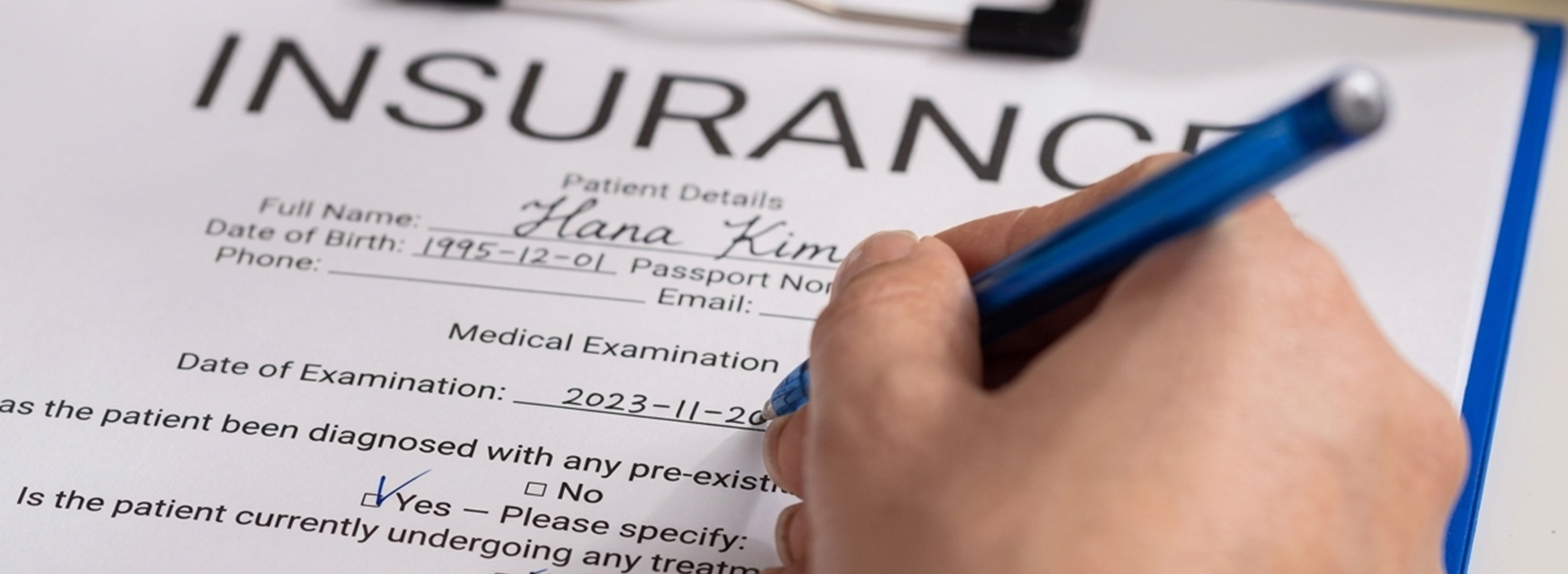

Step 03: Apply Online or Offline (Both Work!)

Online Method (Fastest 15 mins!)

●Visit insurer’s website (e.g., https://adamjeelife.com/)

●Use their premium calculator: enter age, income, sum assured

●Fill basic details (CNIC, contact, nominee info)

●Medical Declaration: Answer health questions honestly (no physical exam for policies ≤ Rs. 5M)

●Pay via JazzCash, Easy Paisa, or card, and get a digital policy instantly.

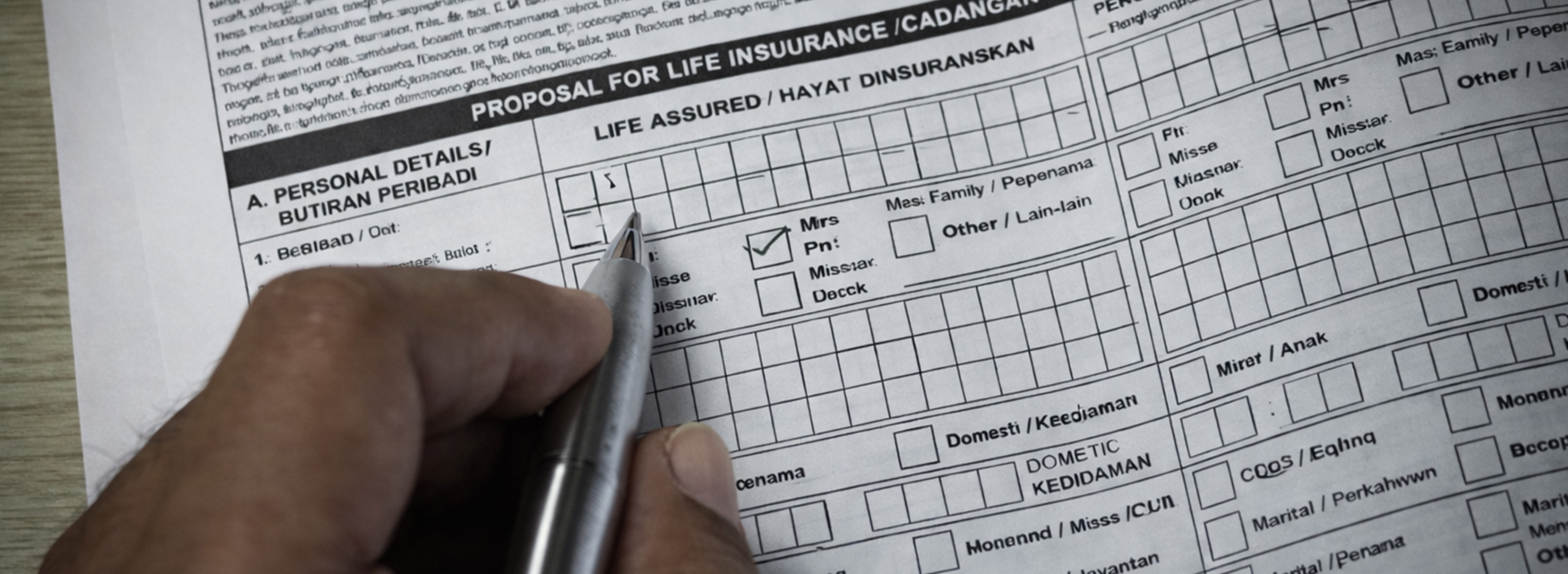

Offline Method (For Complex Cases)

●Visit a branch or call an agent (ensure they’re SECP-registered).

●Required docs: CNIC copy, recent pay slip/bank statement, nominee’s CNIC.

●Medical tests may be needed for >Rs. 5M or ages >45.

Step 04: Nominate Your Beneficiaries (Legally Smart!)

Under Pakistani law, you must name a nominee, but that doesn’t override inheritance (Sharia or Succession Act).

Do This Right:

●Primary nominee: Spouse + minor children (specify % shares: e.g., 60% wife, 20% each child)

●Alternate nominee: Parents/sibling (in case primary passes first)

●Update after major life events (marriage, birth, divorce).

Step 05: Pay & Activate Your Policy

●Payment Modes: Monthly (auto-debit), quarterly, half-yearly, or annual (cheapest).

●Grace Period: 30 days after the due date, coverage stays active!

●Lapse Risk: If unpaid >60 days, policy terminates. Revival possible (with medical check & fees) within 2 years.

Step 06: Keep & Maintain Your Policy

●Store digital copy in Google Drive + physical in a fire-safe box.

●Share details with spouse/nominee (but not passwords).

●Review every 3 years, or after:

●New child/baby

●Home loan taken

●Salary increase (aim to cover 10x income)

Real Talk: What About Claims?

SECP mandates that claims be processed within 15 working days of complete documents.

Documents Needed for Death Claim:

●Original policy bond

●Death certificate (NADRA-attested)

●Nominee’s CNIC + proof of relationship (e.g., Nikah Nama, B-Form)

●Claim form (insurer-provided)

Rejection Reasons

●Misrepresentation (28%)

●Suicide within 12 months (policy clause)

●Lapsed policy

Final Thought: Start Small, Start Now

You don’t need Rs. 20M coverage tomorrow. A Rs. 5 million term plan (≈ Rs. 1,200/month for a 30-year-old non-smoker) is better than zero. Protect your family’s roti, kapra, and makaan one step at a time.

Disclaimer:

All calculations, examples, and illustrations are indicative and provided for general information only. Insurance coverage, premiums, returns, and benefits depend on multiple factors including age, medical history, underwriting assessment, policy structure, and regulatory guidelines. This content does not constitute financial or insurance advice. Individuals should consult a licensed insurance advisor and refer to official policy documents before purchasing any plan.

Frequently Asked Questions:

Can I buy life insurance without a job?

A: Yes, if you have some income (freelance, rental, spouse’s support). Insurers assess “insurable interest.”

Q: Is life insurance halal in Pakistan?

A: Conventional insurance has gharar concerns. Choose SECP-approved Takaful for 100% Shariah compliance.

Q: How long does approval take?

A: Online: Instant for ≤Rs. 5M. Offline: 3–7 days (with medicals).

Q: Can foreigners in Pakistan buy life insurance?

A: Yes, with a valid visa, CNIC/POC, and residency proof. Premiums may be higher.

Q: What documents are required to buy life insurance in Pakistan?

A: These are the following documents required:

- CNIC

- Need Analysis Form

- Proposal Form

- Illustration

- Payment Advice

- Payment Instrument

Declaimer:Please note that the required documentation may vary from customer to customer, and additional documents may be requested as needed.

Eng

Eng  Login

Login